The Week on Wall Street

In a holiday-shortened week, stock prices turned higher as encouraging economic data outweighed an increase in COVID-19 cases and a rollback in economic re-openings.

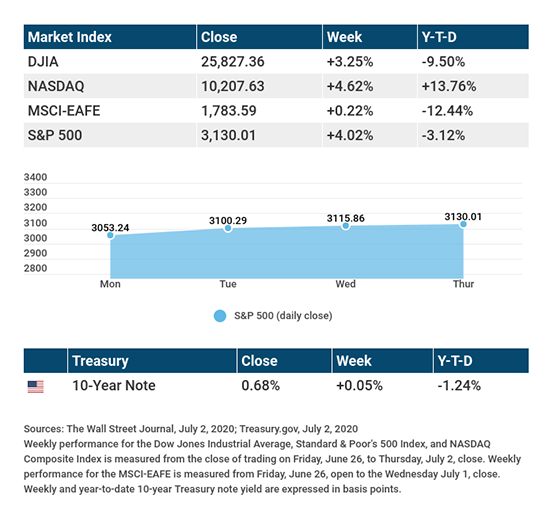

The Dow Jones Industrial Average rose 3.25%, while the Standard & Poor’s 500 increased by 4.02%. The Nasdaq Composite Index gained 4.62% for the week. The MSCI EAFE Index, which tracks developed stock markets overseas, picked up 0.22%.[1][2][3]

The Quarter in Brief

As a new quarter begins, we look back on an eventful second quarter for households and investors alike – a quarter in which the economy took a mighty hit, while the stock market soared. Complying with stay-at-home orders, Americans abruptly cut back on discretionary spending, traveling, and commuting, resulting in a dire scenario for some industries. Unemployment rose as business revenue declined. Fundamental economic indicators saw big swings, and on one trading day, oil prices actually collapsed into negative territory. Homes became easier to finance; though, transactions declined. The Federal Reserve made proactive moves to try and foster a bit more economic stability. While Main Street quieted, Wall Street rallied, sensing that an economic rebound might be starting. The Standard & Poor’s 500 gained 19.95% for the quarter.[4]

What’s to Come

The rally that started in late March continued in the second quarter. Traders were encouraged by better-than-expected earnings in certain industries, positive news about potential COVID-19 treatments and vaccines, and the commitment of the Federal Reserve to address turbulence in the economy and the markets.

All three of the big Wall Street benchmarks recorded their best quarters of the century. The Nasdaq Composite closed at 10,020.35 on June 10, reaching a new milestone. The Nasdaq ended Q2 at 10,058.77; the S&P, at 3,100.29; the Dow Jones Industrial Average, at 25,812.88.[5][6]

As this quarter starts, investors are wondering… is the worst of this recession now behind us? A quick answer may prove elusive. The third quarter may bring more signals that Main Street is bouncing back, but it could also bring a reversal of economic momentum if states continue to halt or reverse phases of opening. For the market to climb higher off of its Q2 melt-up, earnings and economic indicators have to keep showing improvement or least stability. The same goes for COVID-19 case counts. If they keep rising this summer, the bulls could easily be held back.

Jobs, Jobs, Jobs

The ultimate measure of economic recovery is jobs for Americans, and last week, Wall Street got an update from three different perspectives.

First, the ADP (Automatic Data Processing) National Employment Report, which reported private-sector employers added 2.37 million jobs in June. Next, an update on jobless claims, which showed 1.43 million claims, slightly higher than estimates. And finally, the June employment report from the Bureau of Labor Statistics, which showed 4.8 million jobs added, and the unemployment rate falling to 11.1%.Both numbers were better than expected.[7][8][9]

While the employment numbers painted a mostly positive picture, it’s important to remember that the June wave of rehiring was prior to the increase in COVID-19 cases, which has caused some states to revisit their re-opening plans.

THIS WEEK: KEY ECONOMIC DATA

Monday: Purchasing Managers Index (PMI) Services Index. Institute for Supply Management (ISM) Non-Manufacturing Index.

Tuesday: Job Openings and Labor Turnover Survey (JOLTS).

Thursday: Jobless Claims.

Source: Econoday, July 2, 2020

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

THIS WEEK: COMPANIES REPORTING EARNINGS

Tuesday: Paychex (PAYX), Levi Strauss (LEVI).

Wednesday: Bed, Bath & Beyond (BBBY).

Thursday: Delta Airlines (DAL), Walgreens Boots (WBA).

Source: Zacks, July 2, 2020

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.

[1] The Wall Street Journal, July 2, 2020

[2] The Wall Street Journal, July 2, 2020

[3] The Wall Street Journal, July 2, 2020

[4] CNBC.com, June 30, 2020

[5] CNBC.com, June 30, 2020

[6] The Wall Street Journal, June 30, 2020

[7] MarketWatch, July 1, 2020

[8] CNBC, July 2, 2020

[9] The Wall Street Journal, July 2, 2020