The overhang of bumping against the federal debt ceiling was lifted last week with an agreement to extend the debt ceiling through early December, helping propel stocks to a weekly gain.

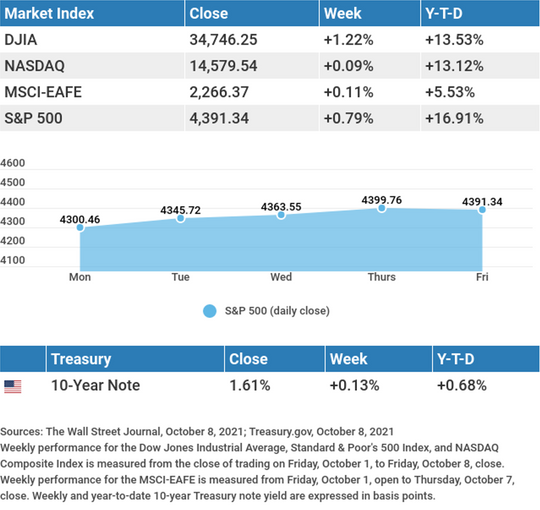

The Dow Jones Industrial Average increased by 1.22%, while the Standard & Poor’s 500 added 0.79%. The Nasdaq Composite index gained 0.09%. The MSCI EAFE index, which tracks developed overseas stock markets, was flat (+0.11%).1,2,3

Debt Ceiling Concerns Evaporate, for Now

After suffering losses on concerns over delays with raising the federal debt ceiling, stocks rebounded as the Senate moved toward finalizing a debt ceiling agreement. While the agreement is only a short-term solution, it was enough to embolden investors to buy stocks.

The week’s rally ran out of gas on Friday, however, on a surprisingly weak employment report. Though the debt ceiling was the dominant concern in the markets last week, the market grappled all week with the headwinds of higher energy prices, rising bond yields, inflation, and less robust economic growth.

Fuzzy Employment Picture

Employment remains a confusing and unpredictable element of this post-pandemic economic recovery. Automated Data Processing’s employment report showed private sector jobs rose by a robust 568,000. This hiring surge may have been aided by the end of extended unemployment benefits and the return of children to school.4

This improving labor outlook was reinforced the following day as weekly initial jobless claims fell below their four-week moving average, while continuing claims fell by nearly 100,000. The employment report on Friday was a different story. The economy added a disappointing 194,000 jobs, making September the slowest month for job growth this year. The unemployment rate declined to 4.8%, while an increase in wages generated inflation worries.5,6

This Week: Key Economic Data

Tuesday: JOLTS (Job Openings and Labor Turnover Survey).

Wednesday: Consumer Price Index. FOMC (Federal Open Market Committee) Minutes.

Thursday: Jobless Claims.

Friday: Retail Sales. Consumer Sentiment.

Source: Econoday, October 8, 2021

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

This Week: Companies Reporting Earnings

Wednesday: JPMorgan Chase (JPM), Goldman Sachs (GS), Delta Airlines (DAL), BlackRock, Inc. (BLK).

Thursday: Wells Fargo & Company (WFC), UnitedHealth Group (UNH), Citigroup, Inc. (C), Walgreens Boots Alliance, Inc. (WBA), Morgan Stanley (MS).

Friday: J.B. Hunt Transportation, Inc. (JBHY), The PNC Financial Services Group, Inc. (PNC).

Source: Zacks, October 8, 2021

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.