Stocks ended mixed last week amid the outbreak of hostilities in the Middle East and higher-than-expected inflation data.

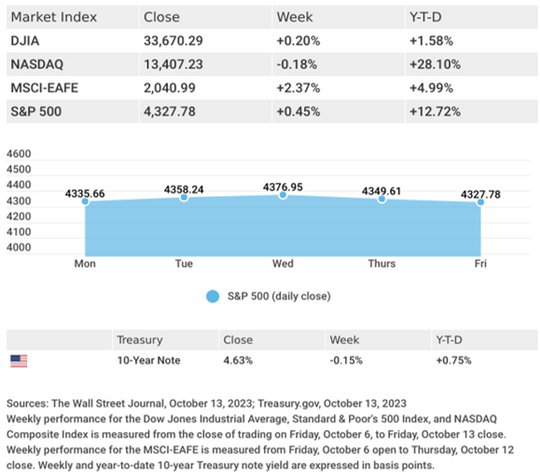

The Dow Jones Industrial Average gained 0.20%, while the Standard & Poor’s 500 rose 0.45%. But the Nasdaq Composite index slipped 0.18% for the five trading days. The MSCI EAFE index, which tracks developed overseas stock markets, advanced 2.37%.1,2,3

Inflation Hurts Sentiment

Stocks exhibited remarkable resilience in the face of a surprise attack on Israel and hotter inflation data than investors expected. Stock prices initially buckled on the breakout of hostilities in the Middle East. Still, they rallied in afternoon trading as investors gained optimism that the war may not spread to other countries. Oil and defense stocks rose sharply, while airlines fell.

Stocks continued to advance into Wednesday as falling bond yields and a retreat in oil prices overcame the disappointment of an elevated wholesale inflation report. When consumer prices also came in higher than anticipated by Wall Street, stocks moved lower in response to higher bond yields. The weakness continued into Friday on a bump in consumer inflation expectations despite a solid start to a new earnings season.

PPI, CPI Updates

The disinflationary trend appears to be stalling if the inflation numbers are any indication. September’s producer price index (PPI) came in higher than expected, rising 0.5% versus a forecast of a 0.3% increase, while the year-over-year increase of 2.2% was the most significant jump since April. The driver of last month’s hop was in goods, which surged 0.9%.4

Consumer inflation data followed, which also came in hotter than forecast. The Consumer Price Index (CPI) rose 0.4% in September and 3.7% year-over-year above the forecast of 0.3% and 3.6%, respectively. The news on core inflation was a bit more comforting, rising in line with expectations.5

This Week: Key Economic Data

Tuesday: Retail Sales. Industrial Production.

Wednesday: Housing Starts.

Thursday: Existing Home Sales. Jobless Claims. Index of Leading Economic Indicators.

Source: Econoday, October 13, 2023

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

This Week: Companies Reporting Earnings

Monday: The Charles Schwab Corporation (SCHW)

Tuesday: Bank of America Corporation (BAC), Johnson & Johnson (JNJ), Lockheed Martin Corporation (LMT), The Goldman Sachs Group, Inc. (GS), Prologis, Inc. (PLD), J.B Hunt Transport Services, Inc. (JBHT)

Wednesday: Netflix, Inc. (NFLX), Tesla, Inc. (TSLA), The Procter & Gamble Company (PG), United Airlines Holdings, Inc. (UAL), Abbott Laboratories (ABT), Morgan Stanley (MS), Elevance Health, Inc. (ELV)

Thursday: AT&T, Inc. (T), Intuitive Surgical, Inc. (ISRG), Blackstone, Inc. (BX), CSX Corporation (CSX), Union Pacific Corporation (UNP), Freeport-McMoran, Inc. (FCX)

Friday: SLB (SLB), American Express Company (AXP)

Source: Zacks, October 13, 2023

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.